An example of our work in Operations

How to choose between different in-house production alternatives?

An example of our work in Operations

All companies with production need to ensure that their manufacturing footprint is a true source of competitive advantage. The following example – taken from our direct experience with a key client of ours, a major player at global level in the Industrial arena – very well illustrates how complex, and at the same time how powerful, dealing with this business issue can be. The key objective of our client was to define which of two very different manufacturing platforms was the best one for them: considering both the detailed financial and organizational aspects, as well as the fit with their long run strategy.

Let’s first summarize the basics of what we are talking about: Polyolefin plastomers/elastomers, mostly metallocene-catalyzed ethylene-co-α-olefins, densities < 0.91 g/cm3

- Copolymers comprising ethylene (or propylene) with alpha-olefins (butene, hexene or octene) produced using metallocene catalyst

- Approximately 65% ethylene or propylene and 35% of alpha-olefin

- Plastomers have densities ranging 0.88 to 0.91 g/cm3

- Sometimes they are referred as VLLDPE (Very Linear Low Density PE)

Plastomers bridge the gap between thermoplastics and elastomers and as such combine many of the physical properties of a rubber with the processing advantages of a thermoplastic, hence their name Plastomers.

There are two alternatives to produce Plastomers:

- Catalloy based technology

- Lupotech G technology

To define the best manufacturing footprint for our client, we also assessed the global industry of the Plastomers. In particular, the market is an expansion phase, with key Supply&Demand drivers:

- Over 1800 kt of Plastomer capacity including existing and planned expansions (all new capacity in Asia Pacific

- Demand to be about 900 kt (risk of over capacity). Asia Pacific: 50% of the capacity & 28% of the demand

- High market growth of existing applications (auto, film/packaging, consumer goods, etc.)

- Utilization of competitive proprietary technology for production

- Capability to innovate new products to remain competitive in the market

- Product development resources to innovate new products for new applications

- Technical-economic benefit compared with other competing materials such as SBC and PVC

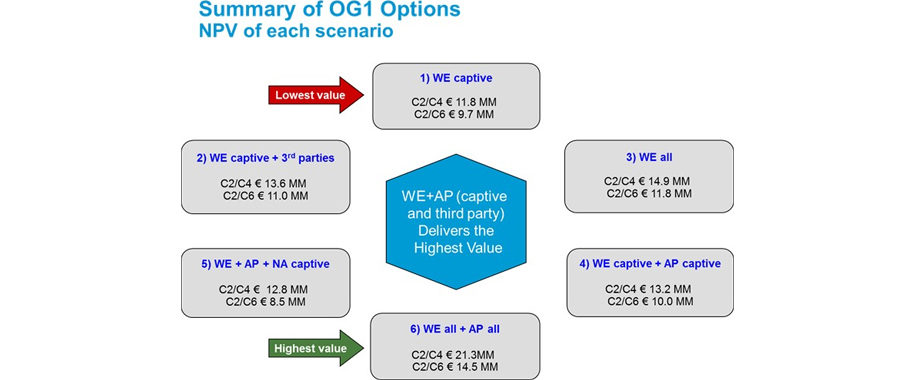

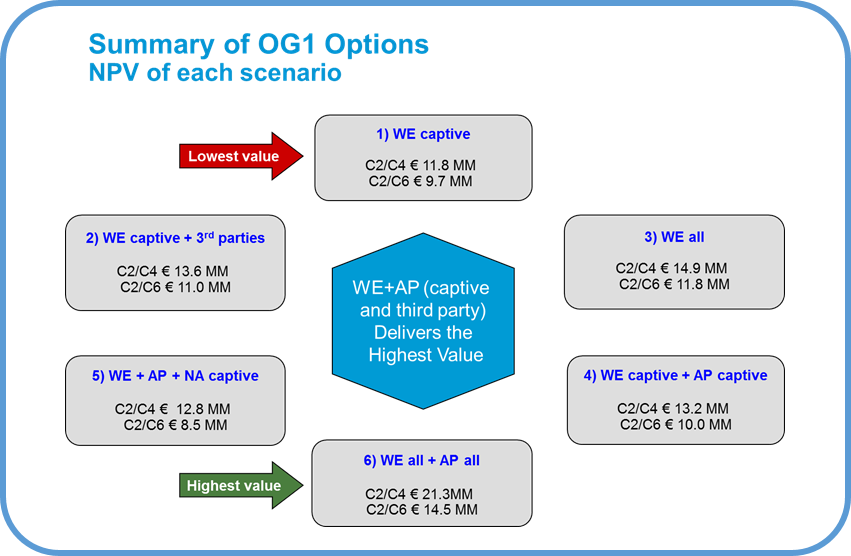

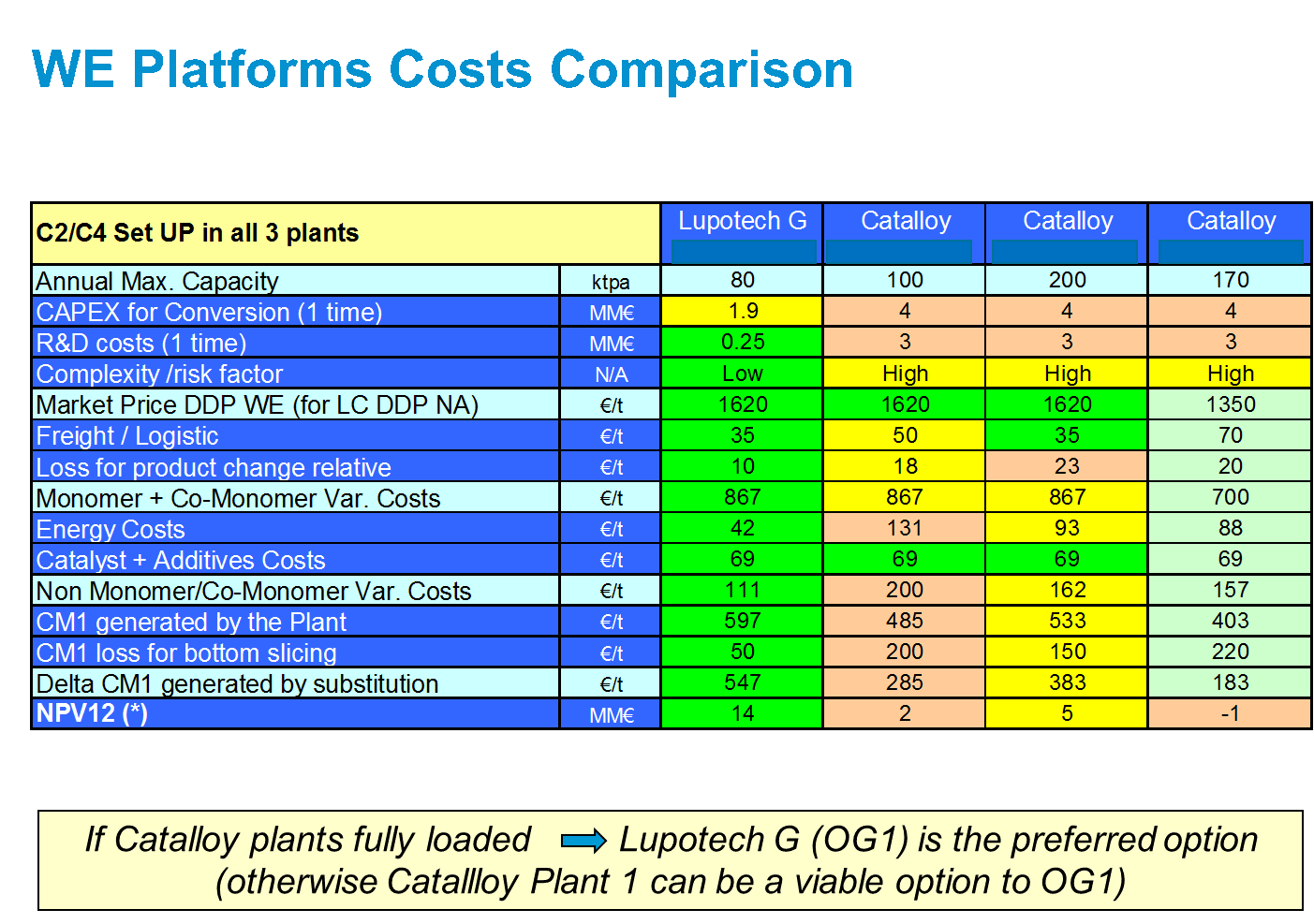

We then thoroughly assessed the detailed economics of the different solutions.

We used our detailed analysis and competences to assess the financial aspect of the alternative manufacturing platforms.

By combining together all the pieces of analysis that we performed and leveraging our methodology, we were able to find the best solution for our client.